As a FIRE investor using individual stocks as a part of my portfolio, not every company I take a position in is going to end up profitable. Often companies I purchase go nowhere, or just remain in a relativley narow band for a long time. Given my goal of early retirement, I don’t really have the patience for unprofitable or flat positions.

In the past week, I sold most of my position in Beyond Meat. I had bought it back in late June Early July of last year between $136 and $151 per share. Then the stock flat until a brief pump in October, followed by a return slightly below where I purchased it. Finally, Thursday last week, the stock jumped to a point where I could in fact sell it profitably, and got rid of it making a profit of $35. The company announced a venture with Taco Bell that caused it to pop. I probably still lost accounting for inflation, still, $35 beats a sharp stick in the eye..

Should I have sold this, maybe, maybe not. The stock was sticking to a range fairly close to what I originally purchased it at, if I am shooting for an aveage return of 10%, this will not get me there. Additionally, I still have a small position in my IRA, so if there is a bigger bounce in the coming weeks, I’m not entirely out of it.

I originally bought Beyond Meat back in June last year in the early days of the pandemic. Back then our supply chains were breaking. People were stockpiling toilet paper, the virus was rampaging through the meat packing plants. As the worlds population continues to demand more beef, how can we keep up with the demand given the amount of resources taken by the cattle industry, where it takes 13 pounds of feed to produce 1 pound of beef. Not to mention the greenhouse gas emissions produced by cow farts. This rate of resource consumption isn’t sustainable.

Beyond Meat’s plant based meet products may very well be a way out of this conundrum, which is why I first purchased the stock. Though I continue to believe this, looking back now, I do now see specific problems with BYND.

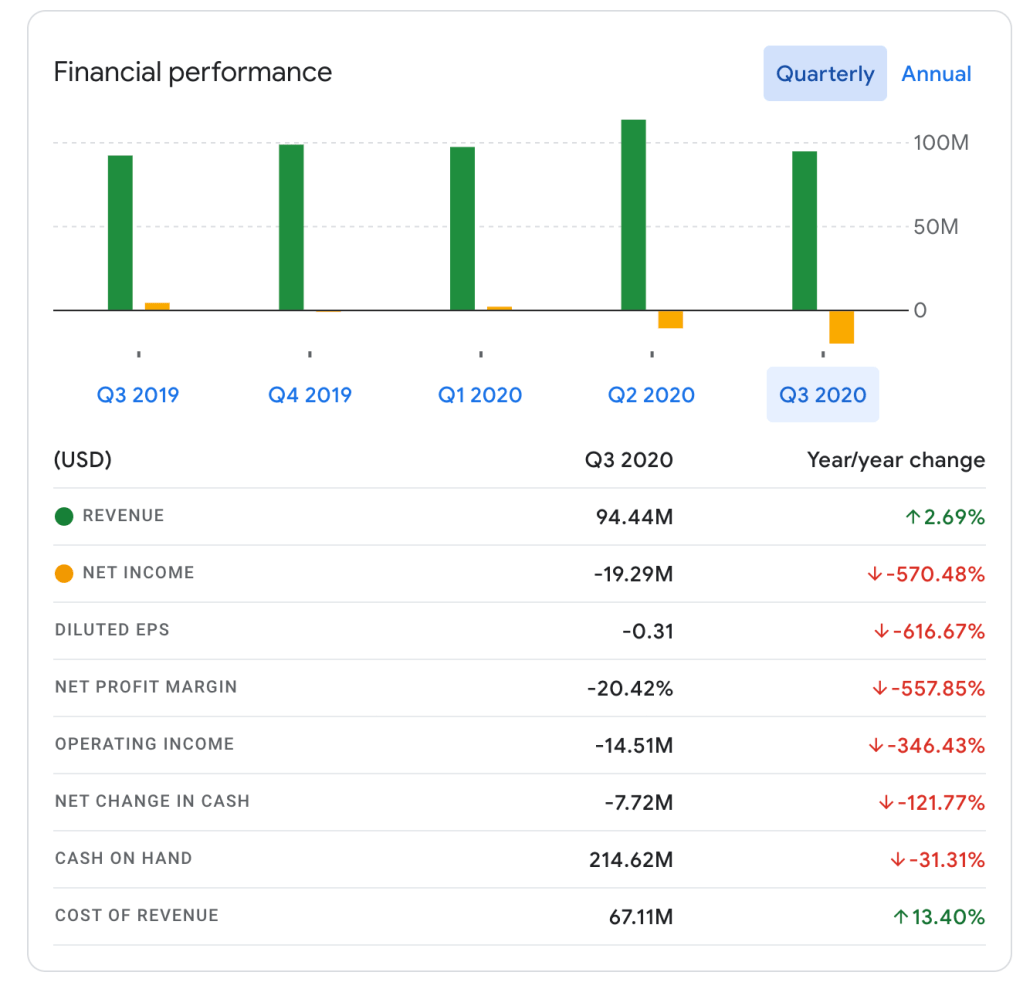

For starters, the company was founded in 2009, over 10 years ago now, they went public back in 2019, yet they continue to lose money like a startup. Last quarter the company lost nearly 20MM, a decline of over 500% from the last year, yikes.

Just browsing through some of the headlines in Google Finance might be indicative of some of the problems, for instance just last week they signed a lease for a big new office, as the rest of the office market contracts due to more and more people working from home due to the pandemic. They say this will allow house three to four times the R&D people over their current facility, which I read as ‘we anticipate losing a lot more money in the coming years to pursue growth‘. For a company like BYND, R&D seems like it would be important for them to maintain a competitive advantage in an industry with low barriers to entry. However, after 10 years, the days of sacrificing profitability in the name of R&D should be behind it. Additionally, as larger, more established players enter the industry, such as Conagra, can BYND really compete with such scale and deep pockets.

I am both an environmentalist and a capitalist, two beliefs that are at times in conflict with each other. Capitalism’s unquenchable drive towards growth no matter what is not sustainable from an environmental perspective. Yet, being a FIRE investor requires me to live off the capital gains and dividends from stock prices continuing to go up.

There are plenty of environmentally sustainable opportunities which can generate gains, just look at the growing set of ESG funds such as ICLN, an ETF which has returned 147% over the past year.

If I go into the holdings of ICLN, it’s mostly made up of smaller companies, which as an individual investor, I am not necessary be aware of. Looking at the top 10 holdings, the only company I know of is the number 10 holding, First Solar, FSLR.

First Solar was a company that was part of my original FIRE portfolio back in the late 2000’s, I have been in and out of it at various times since then. Most recently I sold the company back in May 2019, and have been keeping an eye on it since. The company had a rocky start back after its IPO, going at one point to nearly $300 per share, then after the ’08 financial crisis settling in a range of around $50. Over the past year, the stock has been on a bit of a tear, going back into the $90’s.

Sure, I could buy each of the top 10 stocks in ICLN individually, picking and choosing the ones I think will end up being winners. But this method is generally unproven, as past performance is no guarantee of future results, and what looks like a winner now may not be a winner a year from now. For that matter, the whole trend over the past couple of years towards ESG could in fact go away, though personally I think that seems unlikely given an incoming Biden administration. Then again, I really have no financial training, and at the best just conjecturing on market performance, with a little data to back me up.

Now that trading has resumed after last holiday weekend, I have taken some of my cash from BYND and moved it to ICLN.

Disclaimer: Investing involves risks, and nothing in this post should be construed as financial advice. Risk of investments includes the loss of principal, which I can’t assume liability for. Please consult with an actual financial advisor for advice.

Leave a comment